Personal consumption growth has materially moderated, but private wage growth rebounds

While a major deceleration in real disposable income growth has now led to a significant slowdown in personal consumption growth, an increase in private industry wage growth complicates the outlook.

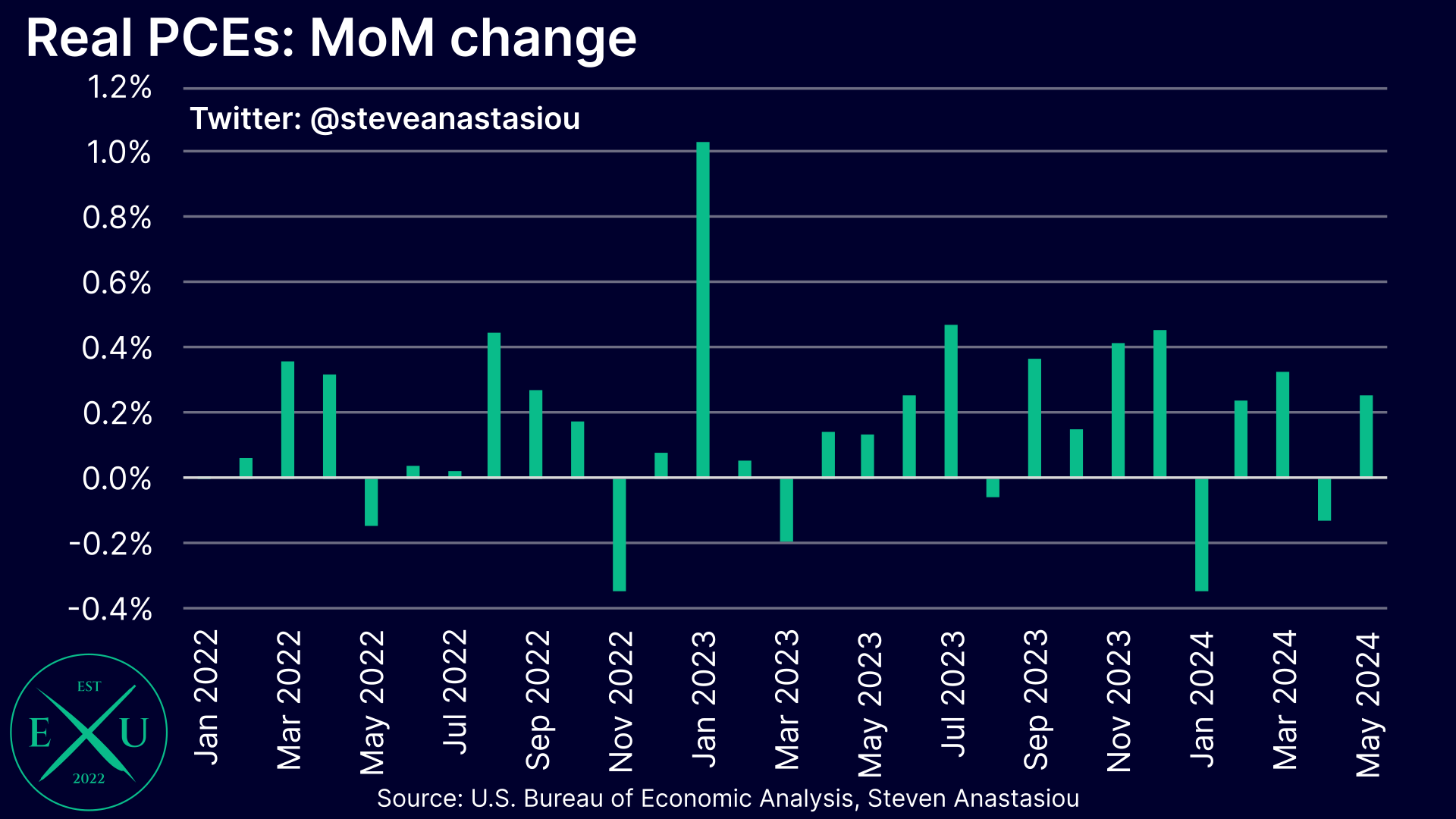

Consumer spending growth slows as moderating disposable income growth begins to take more of a toll

Following a downwardly revised change of -0.13% in April, real personal consumption expenditures (PCEs) grew by 0.26% in May.

Downward revisions saw April’s 3-month annualised growth rate revised down to 1.8%, from 2.7% previously. 3-month annualised growth remained at 1.8% in May.

6-month annualised growth was revised down to 1.9% in April (from 2.5% previously) and fell to 1.6% in May.

YoY growth rose to 2.4%, up from a downwardly revised figure of 2.3% in April (previously 2.6%).

After a period of relatively strong real PCE growth in 2H23, the latest data indicates that the slowdown in consumer spending growth that was seen in 1Q24 has continued into 2Q24.

Given the significant slowdown that’s been seen in real disposable income growth (1.1% YoY in May vs 3.8% in December) and a savings rate that remains well below its historical average (3.9% vs the 2015-19 average of 6.2%), a slowdown in real PCE growth has been expected and something that I have been articulating — including in my latest US Economic Review and Outlook.

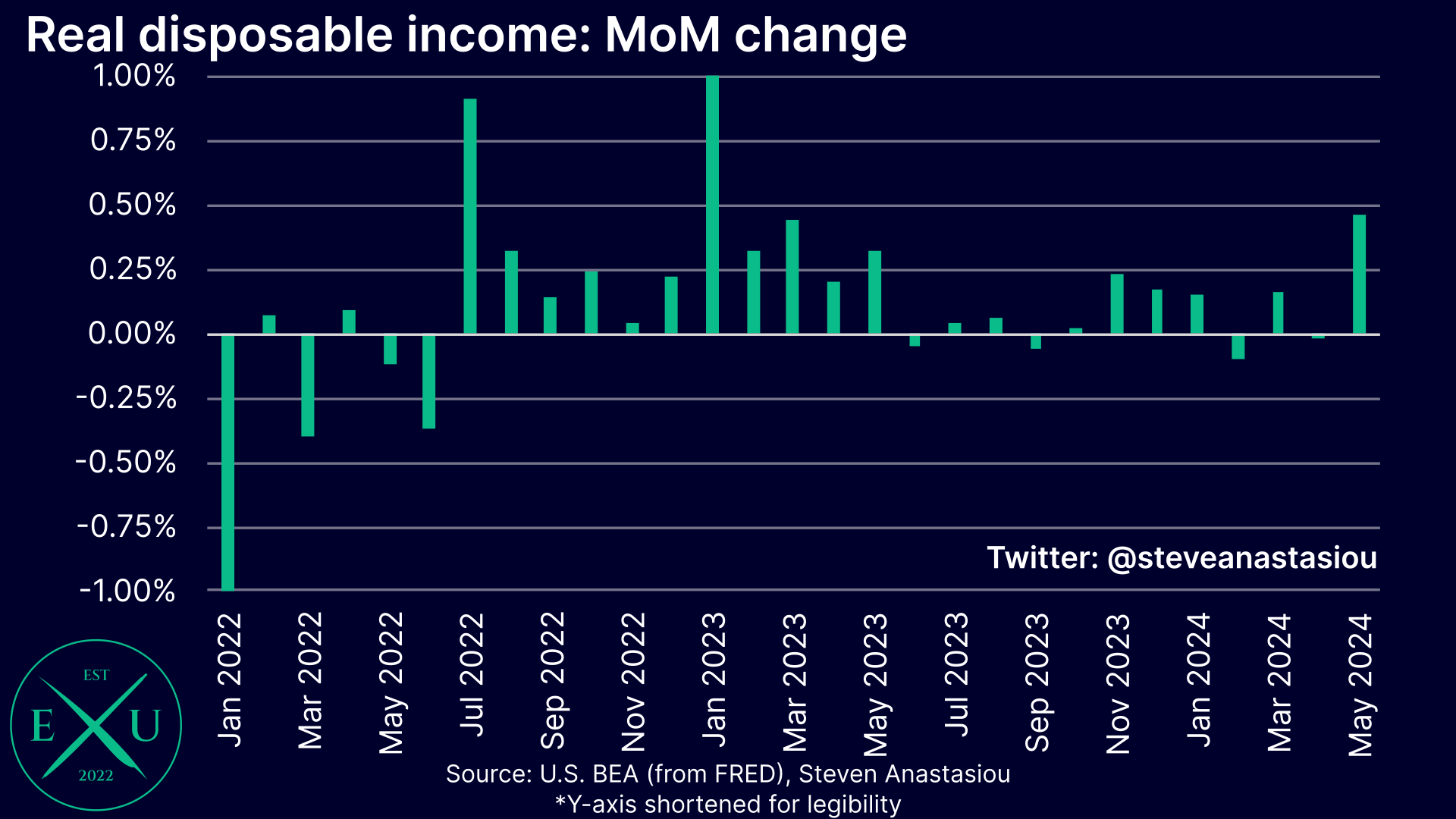

Though disposable income growth bounces back in May, aided by wages and salaries and MoM deflation

Despite a broader trend of decelerating real disposable income growth, MoM growth accelerated in May, rising by 0.46%, the largest increase since January 2023.

In addition to being supported by MoM deflation (headline PCE Price Index growth was -0.01% MoM vs 0.26% in April), growth was driven by a 0.64% MoM increase in employee compensation.