Digging deeper into Q4 US GDP reveals a weak picture

The advance estimate for 4Q22 US GDP came in at 2.9%. While this was a moderation from the annualised growth rate of 3.2% for 3Q22, it represented an upside surprise to consensus estimates, which had forecast growth of 2.6%.

As opposed to indicating a recession is now happening, or is set to imminently occur, the headline GDP number instead suggests that the US economy is doing relatively well. A deeper dive into the GDP numbers suggests otherwise — let’s explore.

Real spending on goods turns positive but remains relatively weak

After three consecutive quarters of declines, real spending on goods rose in 4Q22, but growth remained tepid, increasing by an annualised rate of 1.1%. Breaking this down further, real durable goods spending increased by just 0.5%, following two quarters of declines.

Durable goods spending was supported by a rebound in spending on motor vehicles and parts. Real spending in the other durable goods category fell by 10.1%.

Nondurable goods spending, which rose 1.5%, was supported by an increase in real spending on gasoline, which rose at an annualised rate of 2.6%.

Nominal goods spending falls: a warning for corporate sales

On a nominal basis, goods spending fell in 4Q22 for the first time since 3Q21. This is a marked change from the strong growth recorded from 4Q21-2Q22.

While changes in nominal GDP get less attention than the inflation adjusted numbers, it’s nominal rates of change that are important for corporate revenue. Should the huge deceleration in nominal goods spending that has now reverted to outright declines continue, it will pressure sales revenue for many corporations, and have flow on implications for the stock market.

Services spending growth has decelerated & is being propped up by health care spending

Amidst low growth in spending on durable goods, spending on services has also decelerated significantly, falling from growth of 4.6% in 2Q22, to 2.6% in 4Q22.

If health care spending is excluded (which is a metric that is more non-discretionary, and which could be argued is not a good thing, as it can indicate an aging/less healthy population), the decline in growth is even more stark, with annualised PCE services ex-health care growth falling to 2.2% in 4Q22. This is the lowest reading since 2Q20, which was in the midst of COVID shutdowns.

Fixed investment tumbles to recessionary levels

Due in large part to a HUGE decline in annualised residential investment of 26.7%, overall fixed investment fell by 6.7% in 4Q22. This was the 3rd straight quarter of large declines in fixed investment. Outside of the worst of the COVID period, 4Q22 was the largest decline recorded since the GFC.

As can be seen in the chart below, declines in fixed investment of this magnitude have generally been consistent with a recession as per the NBER definition.

Net exports support GDP, but also provide a recessionary signal

Given that durables growth was modest, services growth saw further moderation, and fixed investment tumbled, large contributors to 4Q22 GDP growth included:

the volatile components of net exports and changes in private inventories; and

increased government consumption expenditures.

Given that we know that the government has an insatiable appetite for spending their constituents money, and that this is likely to continue, it is the former two components that I will now focus my attention on.

For the 3rd straight quarter, net exports delivered a significant increase to GDP. While this may seem positive, the GDP benefit in 4Q22 was delivered solely by lower imports, as exports also declined, falling by 1.3%.

This combination spells trouble for future GDP growth. Why? Firstly, lower exports suggest reduced global demand. Though it is important to caveat the 4Q22 number by noting that exports are a volatile data series, and China’s reopening is likely to provide some support to exports moving forward.

Of more concern at this stage for the US’ future economic outlook, is the trend in its imports, where a clear trend of decelerations/declines are now in place. While in isolation this supports GDP growth (to the tune of 71bps in 4Q22), we must remember that the US has not suddenly onshored a huge amount of manufacturing. Imports are instead declining because US demand is falling — drastically reduced imports thus suggest a weak economy.

Again, this can be seen in the historical data, with prolonged declines in imports often being associated with recessions. This relationship has been particularly true since the 1980s, at which time the US began to rely more heavily on imports of durable goods, as opposed to domestic manufacturing.

Inventories rise after a significant drawdown & continued modest PCE growth

Another key driver of GDP growth during 4Q22 was a large increase in inventories, which contributed 146bps to the overall 4Q22 GDP growth rate of 2.9% (i.e. ~50% of the total).

This comes after private inventories contributed two consecutive large declines to quarterly GDP, and as PCE growth remains modest — particularly so for durable goods.

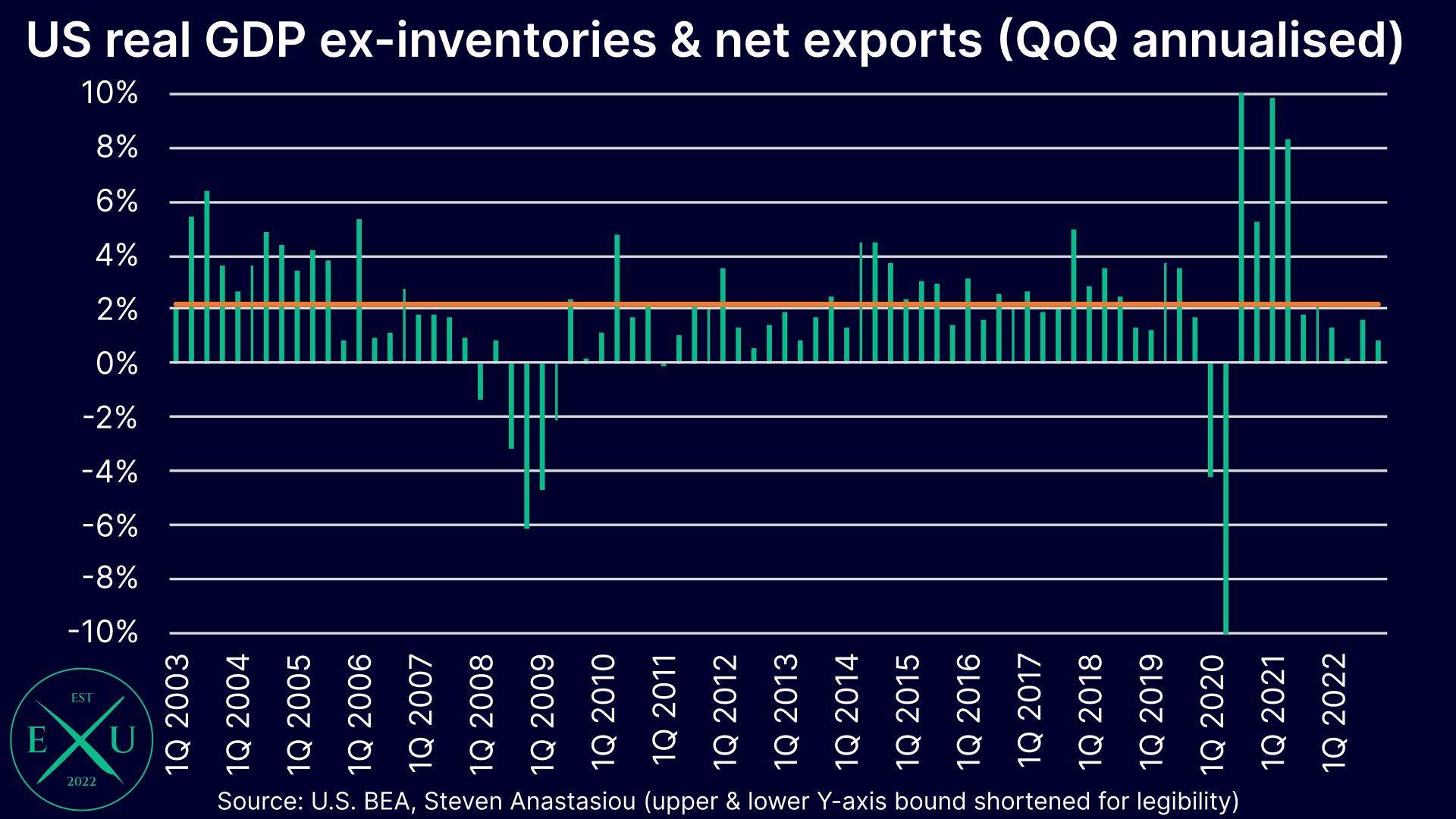

GDP excluding volatile net exports & inventories points to reasons for concern

Excluding the volatile net exports & inventories components, which also happen to provide conflicting signals on the health of the US economy, reveals a weak underlying GDP picture. Annualised growth in 4Q22 on this metric was just 0.9%, down from 1.6% in 3Q22, and well below the average growth rate of 2.2% that has been recorded since 2003.

Unlike for headline GDP, the US didn’t see negative growth on this metric across 2022, with the 1Q & 2Q22 declines in real GDP impacted significantly by changes in net exports and inventories respectively. Instead of a rebound from negative numbers, this measure of the US economy remains weak.

Continuing to expect a 2023 US recession

In summary, a deeper dive into the US’ latest GDP report suggests economic weakness.

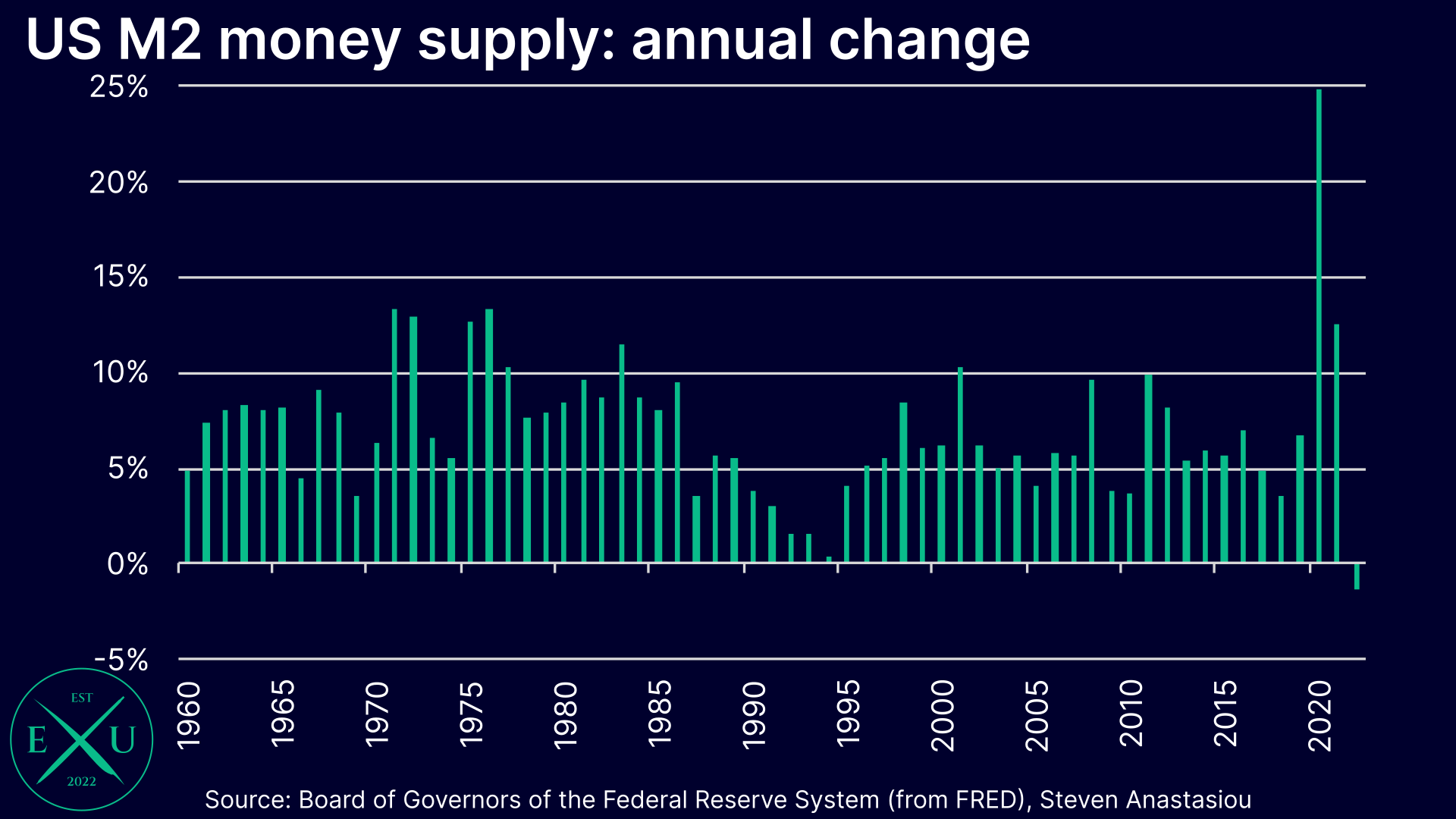

With the US’ M2 money supply recording its first annual decline in 2022 for at least 60+ years, and the Fed continuing to tighten in the face of this, I am not surprised to see that the underlying GDP picture remains weak.

Just as the surge in M2 from federal government stimulus and an extremely loose Fed caused GDP to surge, I continue to believe that the most aggressive tightening from the Fed in 40 years, will likely result in the US experiencing a severe recession during 2023.

Thank you for continuing to read and support my work — I hope you enjoyed this latest piece.

In order to help support my independent economics research, which aims to provide not just hedge funds & asset managers with access to institutional grade research & insights, but ordinary people, please like and share this article.

If you haven’t already, make sure to subscribe so that you don’t miss an update — it’s free!

When do you think employment starts to drop? That’s the only piece of the macro puzzle that remains stubbornly strong. Last I checked, there was still a big gap between open jobs and jobseekers and my intuition is that jobless claims won’t markedly rise until that gap closes. Secondarily, I think that the lower oil and gas prices are keeping the economy strong, but that will reverse if oil prices rebound. Love to hear your thoughts.