Deciphering the outlook for services prices

This research piece unpacks where services prices are likely to head, including when they may fall to a level that will allow CPI growth to sustainably return to 2% YoY.

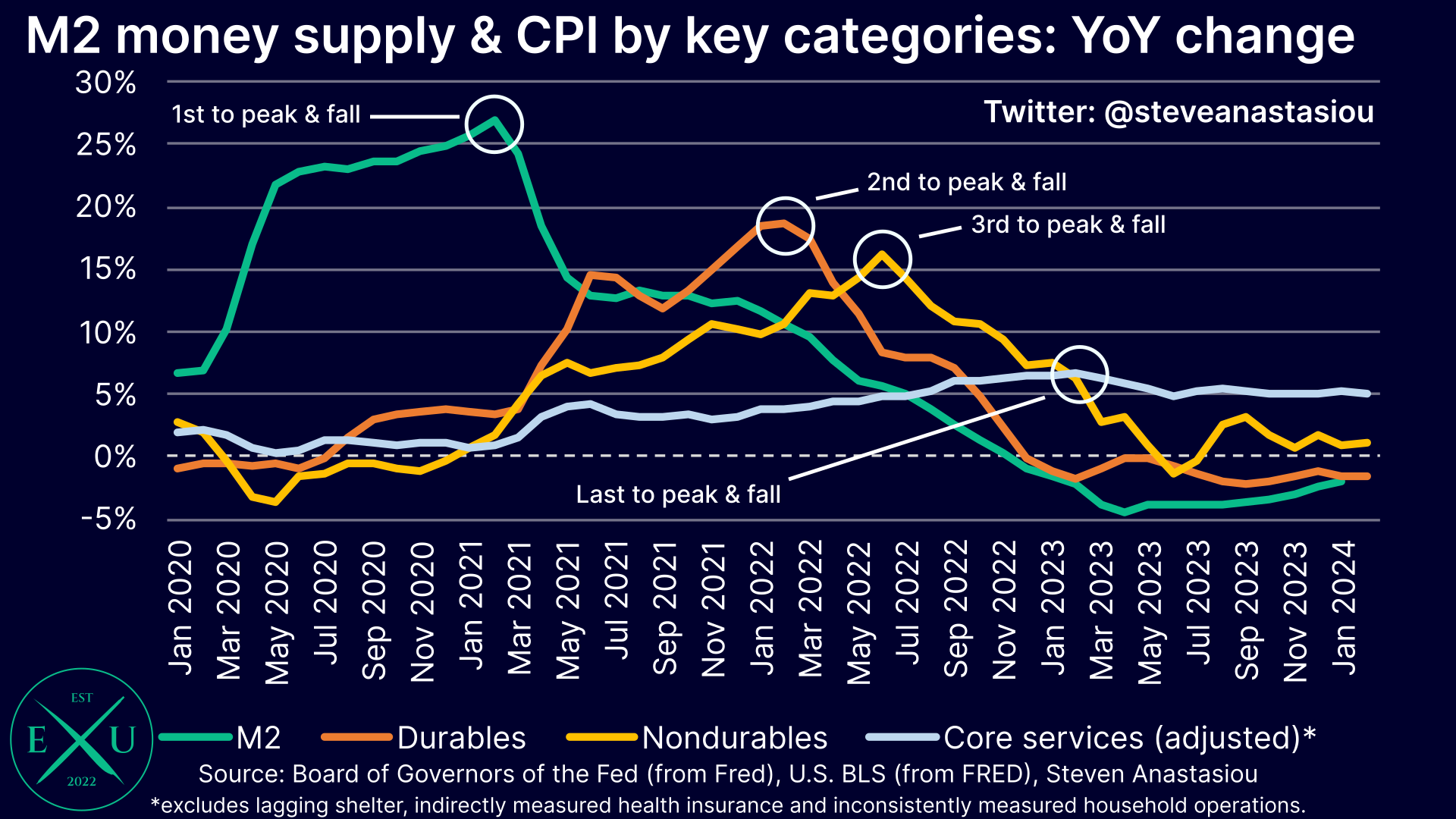

US disinflation has stalled.

The reason? Lagging services prices, which remain materially elevated as the first two phases of the disinflationary cycle (durables and nondurables price disinflation) have already largely completed.

While continued constraints in M2 growth point to little prospect of a second wave of higher inflation, lagging services prices do significantly add to concerns that US inflation may remain above 2% YoY for an extended period.

This concern is emphasised by the fact that the CPI’s lagging owners’ equivalent rent (OER) index has seen relatively little disinflation over the past 12 months, suggesting that extrapolating certain spot market rent indicators may be materially overestimating the extent of shelter disinflation that may occur during 2024.

Attempting to gauge the direction of services prices

Given the importance of services prices to the disinflationary outlook, I intend to release two important pieces on services prices. The first, being this current report, will focus on core services prices more broadly. The second, which I intend to release within the next few days, will focus on the lagging rent based components of OER and rent of primary residence (RPR), and will reevaluate the price outlook for these two components in light of the latest data and broader trends.

The analysis contained within these research pieces will help to underpin my upcoming Medium-term US Inflation Update. This report will include an update to my medium-term US CPI forecasts, as well as an updated analysis on current PCE inflation trends, and the implications for Fed policy. This report is currently scheduled to be released next week.

Let’s now focus on the issue at hand for this research report, being the outlook for core services prices more broadly.

Given that the M2 money supply remains constrained, this suggests that the key question isn’t whether services prices will materially disinflate, but when, and by how much?

In order to try and answer these questions, I will:

unpack the link between services prices and wages;

extrapolate the outlook for wages through a range of leading indicators;

extrapolate the outlook for CPI services ex-energy services price growth via the link to the extrapolated outlook for wage growth; and

explain what the extrapolation of CPI services ex-energy services price growth may entail for the overall CPI.

Beginning with the first point, it’s critical to understand that services prices tend to closely follow wages.

The below chart shows that the Atlanta Fed Wage Growth Tracker and the CPI services ex-energy index have a strong correlation over most time periods — and a particularly strong correlation during the current inflation cycle.