An inversion of M2 and the CPI: a reliable recession signal

With the US' M2 growth decelerating sharply, as opposed to inflation, a significant recession should now be the major concern

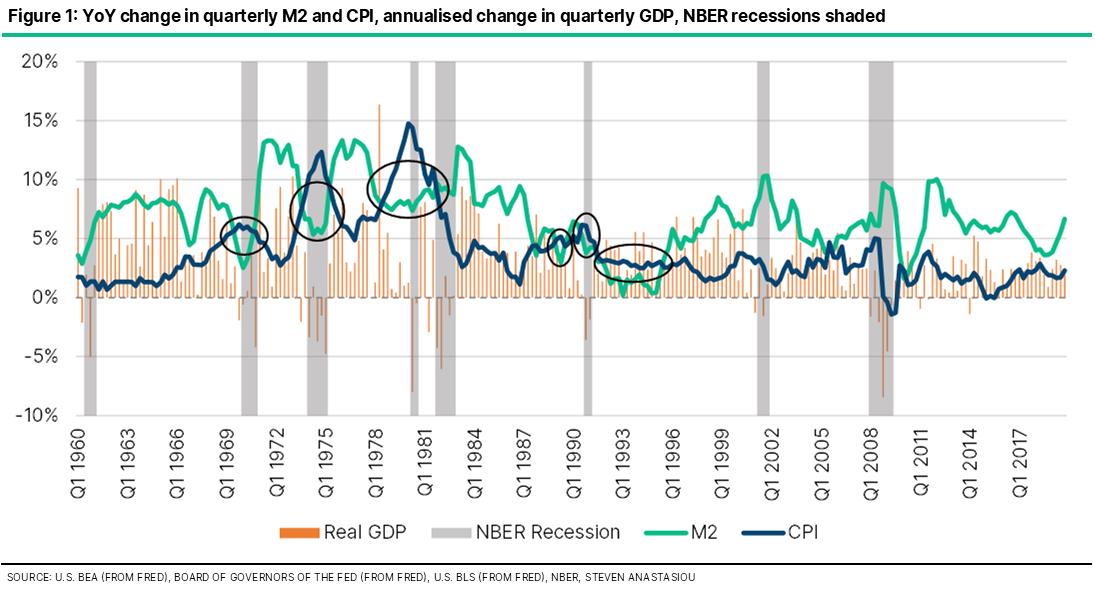

Alongside the US delivering its second consecutive quarter of negative GDP growth in Q2 2022, another key event occurred—an inversion between M2 and the Consumer Price Index (CPI). Though it went largely unnoticed, this is an extremely important event. I define an inversion between the money supply and inflation as occurring when the year-on-year (YoY) growth rate of inflation (i.e. the CPI) increases at a faster rate than the YoY growth rate of M2 (which for the US, is the broadest measure of the money supply provided by the Fed).

When do inversions of M2 and the CPI most commonly occur?

M2 generally increases at a faster rate than the CPI across most time periods. This is largely a result of general improvements in productivity across most time periods, which act to offset the inflationary impact of M2 growth.

Though following periods where there has been an artificial increase in the money supply (which is generally caused by large government deficits financed by the Fed), inversions are likely to occur. I posit that a reliable indicator of an artificial increase in the US’ money supply having occurred, is when YoY M2 growth is above 10 per cent.

An artificial increase in the money supply creates the necessary conditions for an inversion of M2 and the CPI to later occur for two key reasons:

1) The artificial increase in the money supply generally leads to a sharp increase in inflation; and

2) As the artificial increase in the money supply is often a result of temporary measures, spending eventually returns to more normal levels, causing the rate of growth in M2 to fall (usually whilst inflation is simultaneously still rising, as prices generally change with a lag to growth in the money supply).

Why is an inversion of M2 and the CPI a reliable recession indicator?

In order to understand why an inversion of M2 and the CPI is a reliable recession indicator, one must first understand what happens during an artificial expansion of the money supply, which often precedes an inversion of M2 and the CPI.

While a detailed analysis of the impacts of an artificial expansion of the money supply is cause for its own separate research piece (and of which I have written about more expansively in this report), the key point that one needs to understand, is that when the money supply is artificially expanded, it creates inflationary price pressure, but it does so with a lag.

Why do prices lag an artificial change in the money supply?

If we use the COVID period as an illustration, the drastic increase in the money supply during this time period was driven by large government deficits that were financed by the Fed. Amongst other things, the large government deficits occurred on account of direct stimulus payments to individuals, and increases to unemployment benefits.

Once individuals received these income supplements, their increased stock of money meant that in isolation, they were now more likely to increase their demand for goods and services. Many retailers, such as electronics, home appliances, and furniture retailers, thus benefited greatly. Owners of these businesses now saw their incomes rise, allowing them to increase their consumption, and/or reinvest into expanding their businesses. As this process continued, more and more businesses saw an increase in demand, and eventually this caused a broad increase in demand, and prices across the economy.

Now while this meant that inflation eventually rose, it did not occur immediately upon the new money being printed. Instead, it took time for funds to be distributed to recipients. It took further time for the initial recipients of stimulus checks to spend them. It took further time still, for the second order recipient to spend their additional income, and so on, until the new money reached a sufficiently large portion of the economy to create broad price pressures. It also took time for businesses to be confident enough that the higher demand would continue, and that they should thus raise their prices. As opposed to an overnight process, this is a process that instead takes place over many months, and for it to fully play out, it may take years. During the COVID period, it took around one year before the initial surge in the money supply (which occurred following the passage of the CARES act in March 2020) resulted in much higher prices.

The impact of prices changing with a lag to the money supply

When the money supply is increased, but prices remain largely the same, there will, in isolation, be an increase in the real demand for goods and services, making the increase in the money supply initially stimulatory. It will continue to be stimulatory until prices eventually rise. Though once prices rise, the level of real demand, all else being equal, will revert to its pre-inflationary level, creating a contraction.

To illustrate, say that an economy contains 1,000 units of goods and services at an average price of $10. All else being equal, if the supply of money increases by 10 per cent, the demand for those 1,000 units of goods and services will rise. Businesses will sell-out of their inventory more quickly, shortages may ensue, and businesses will respond by increasing their inventory and/or production levels. In response to the higher demand, and/or an increase in input costs to raise their operating capacity, businesses will also begin to raise their prices. For simplicity, let us say that there was a direct 1:1 relationship between the increase in the money supply, demand and prices. Eventually, production and prices both rise by 10 per cent, to 1,100 units, and $11, respectively.

Though now there is a problem, as the 10 per cent increase in prices means that despite the supply of money being previously increased by 10 per cent, real purchasing power is now the same as it was before the increase in the money supply had occurred. Businesses then realise that the increase in demand was but a temporary charade, and that much of their additional manufacturing capacity and/or inventory investment was unwarranted (as Target and Walmart, amongst other retailers, are now finding out). These investments become malinvestments—we must remember that an increase in the money supply does not create any real wealth, and today, is nothing but extra digits on a computer. An economic contraction will then result as businesses scale back their output to reflect the new level of real demand (which is, all else being equal, the old, pre-money supply expansion, level of real demand).

I stress the point all else being equal, as in the real world, this is never the case. There will always be changes in the demand for money, and supply-side conditions, meaning that there is unlikely to be a direct 1:1 correlation like that described above. Though whether or not there is a 1:1 relationship between the variables is not the key point. Instead, at whatever ratio it may occur, the key is that there is at least some lag between artificial changes in the money supply, and prices, for it is the lag that temporarily creates an increase in real incomes and demand, which later reverses as prices rise.

An inversion, being the point at which prices rise at a faster pace than growth in the money supply, represents the technical turning point at which a previously stimulatory increase in the money supply, becomes a contractionary pull as prices rise and real demand falls.

The empirical evidence

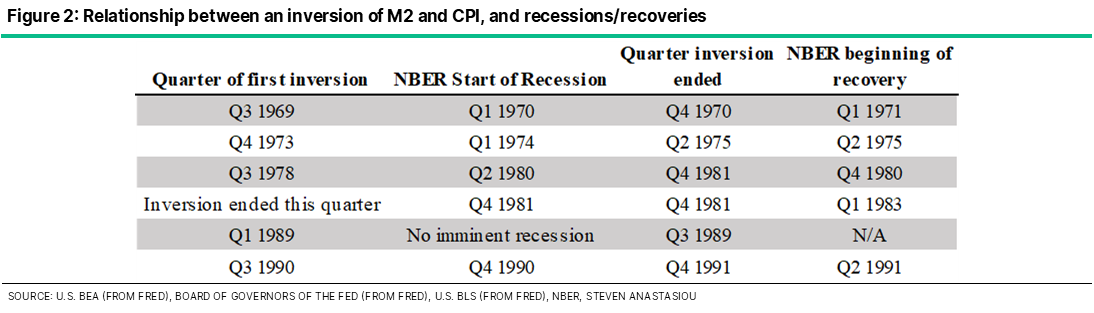

Since 1960, the US has seen six inversions of M2 and the CPI for two consecutive quarters or more. An economic slowdown or recession occurred alongside four of these inversions (Figures 1 and 2 below).

The two periods where an imminent recession or slowdown did not occur was during the 1989 and Q1 1992-Q2 1995 inversions. The 1989 inversion was only brief (two quarters), and a recession followed ~18 months later, one quarter after a follow up inversion. The Q1 1992-Q2 1995 inversion should not be regarded as relevant to this principle as: 1) it followed the 1990/91 recession, meaning there was no need for an economic correction as one had already occurred, and 2) money supply growth during this period was abnormally low, meaning there was no artificial increase in the money supply. The conditions necessary for significant malinvestment to accumulate were thus not present.

Turning our focus to where there was a clear relationship, the 1970-71 recession began two quarters after M2 and the CPI inverted, and the 1974-75 recession began one quarter after M2 and the CPI inverted. The 1980 recession began seven quarters after the Q3 1978 inversion, but growth slowed dramatically shortly after the initial inversion. The subsequent 1981-83 recession occurred just after a brief uptick in the extent of the inversion that was in place since Q3 1978. The 1990-91 recession began one quarter after the Q3 1990 inversion.

Another inversion, another recession?

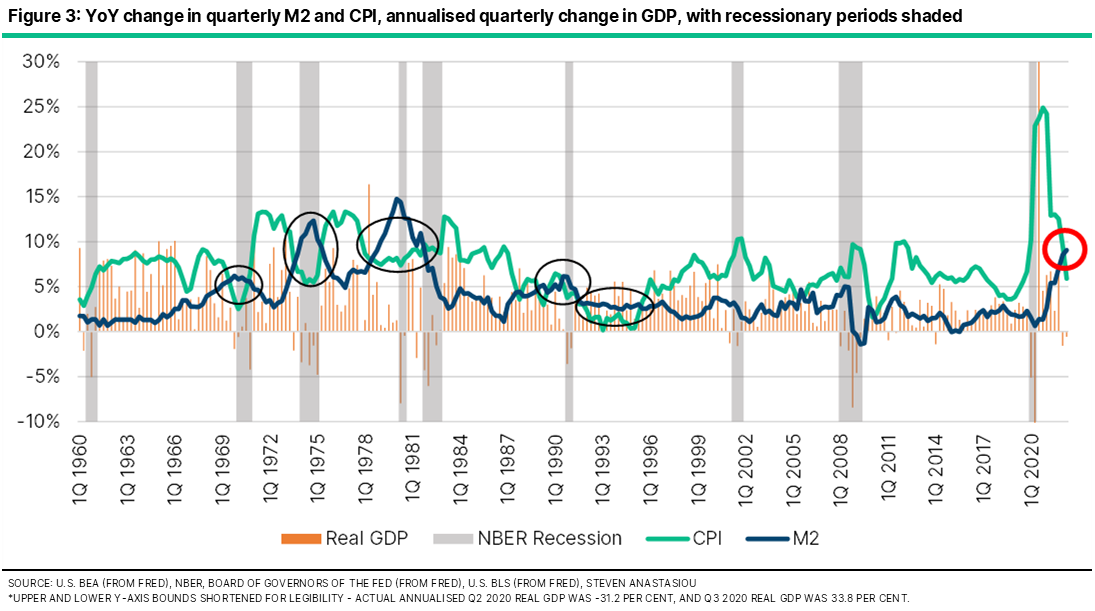

Turning our attention to today, where we can see that a new inversion occurred in Q2 2022 (Figure 3), coinciding with the US’ second consecutive quarter of negative GDP growth. Whilst some will argue whether the US is currently in a recession or not, yet again, an inversion has coincided with negative GDP growth. The inversion between M2 and the CPI has also coincided with real hourly wages falling to below their pre-COVID level (Figure 4).

Flatlining M2 means a significant recession is the key concern

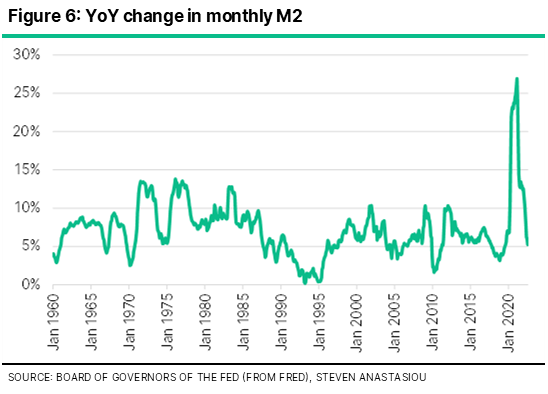

The dissipation of US federal government COVID spending, and an increase in tax revenues on account of rising nominal incomes, has seen a sharp decline in the rolling 12-month federal government deficit (Figure 5). Combined with a continued tightening of monetary policy by the Fed, the US is undergoing one of the sharpest decelerations in M2 growth in its history (Figure 6), with M2 remaining stagnant during 2022.

This is likely to result in YoY M2 growth flatlining by the end of 2022 for the first time in decades, and an extended period of inversion between M2 and the CPI. Instead of inflation, which is likely to fall over time (and potentially even result in deflation if M2 remains stagnant for an extended period), the risk of a significant recession, now firmly takes centre stage.

This is particularly so in light of a Fed that remains hawkish, and who seemingly appears set to repeat its previous mistakes in reverse—that is, after failing to recognise that extreme growth in the money supply would create high inflation, it now seems to have failed to recognise that with M2 flatlining, the hard work on containing inflation has already been done. Just as it took time for the surge in the money supply to create high inflation, it will also take time for the flatlining of M2 to bring down inflation—but all the Fed needs to do is wait. By continuing to tighten monetary policy in the interim, in contrast to previously artificially increasing the money supply, the Fed risks creating an artificial ceiling on M2, magnifying the contractionary pressure of the current inversion, and potentially creating a significant recession. This, as opposed to inflation, is now the much bigger concern.

For those looking for a more in-depth analysis of the US’ current high inflation, the role of money supply growth in causing it, and the outlook for inflation in the US, please follow this link to access my 70-page special report on inflation.